Model Note: The Coherence Signal Called the Cycle. Now the Cycle Has to Earn It.

Thresher Fixed LLC · March 2026

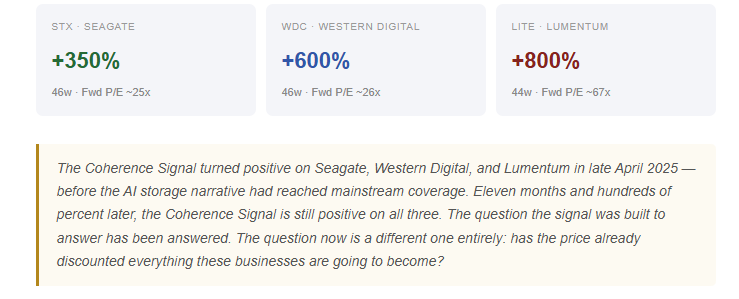

What the Signal Saw First

In late April 2025, Seagate and Western Digital were still being priced as commodity hard disk drive manufacturers. The market had not connected the dots between AI training infrastructure and storage demand. The Coherence Signal turned positive on both names on April 30th — emerging from a selloff, against a backdrop where the broader market was still recovering.

The fundamental story that followed was real and large. AI training at hyperscale is as storage-intensive as it is compute-intensive. Every model run reads and writes enormous volumes of data. The three major HDD manufacturers found themselves reclassified from commodity vendors into critical infrastructure suppliers almost overnight.

Western Digital’s CEO confirmed on an earnings call that the company is sold out for all of calendar 2026 with firm purchase orders from its top seven customers, and that long-term agreements extend to 2027 and 2028. Seagate echoed the same: nearline capacity fully allocated through 2026, demand visibility strengthening into 2027. HDD prices rose 46% in five months. WDC’s hyperscaler AI revenue reached 89% of total sales.

Lumentum is a parallel story in a different layer of the same infrastructure. It makes laser chips and optical transceivers connecting GPUs across racks. Revenue grew 65% year over year. In March 2026, Nvidia invested $2 billion in the company with multi-billion dollar purchase commitments attached — a direct statement about how critical optical interconnect capacity has become to the AI build-out. Lumentum joined the S&P 500 the same month.

The Capex That Makes the Orders Real

The purchase orders sitting behind these three companies are not speculative. They are downstream of the largest coordinated capital deployment in the history of technology. The largest hyperscalers — Amazon, Microsoft, Alphabet, and Meta — have collectively committed to spending roughly $660–690 billion on capital expenditure in 2026, nearly double 2025 levels. Roughly 75% of that — approximately $450 billion — is directed at AI infrastructure: data centers, compute, networking, and storage.

Amazon alone is projected to spend $200 billion, with analysts forecasting it goes cash flow negative on the build-out. Google revised its 2025 capex forecast upward three separate times. Meta’s CEO said explicitly that making a significantly larger investment in AI is “very likely to be profitable.” Capital intensity at some hyperscalers has reached 45–55% of revenue — ratios historically associated with utilities, not technology companies.

WDC’s sold-out 2026 HDD capacity and Seagate’s multi-year allocation agreements are locked to this build-out. The purchase orders extend to 2027 and 2028 because the hyperscalers themselves have committed capex that far out. The storage demand is not a separate bet — it is a direct consequence of a capital war that no major player is willing to lose.

STX, WDC, LITE vs NVDA — weekly price index, March 2025 = 100. Coherence Signal turned positive on STX and WDC April 30th, LITE May 14th.

The Signal Did Its Job. The Question Has Changed.

A Coherence Signal identifies when a structural shift is beginning to show up in price. That is what happened here. What it cannot tell you is whether the structural shift warranted has been fully priced. At some point the answer to “is this still cheap relative to what it’s becoming” flips. That is a valuation question, not a signal question.

STX and WDC present the cleaner case. On forward earnings — which incorporate the AI-driven revenue trajectory — STX trades at roughly 25x and WDC at 26x. STX’s 10-year average P/E is 18x. Against confirmed purchase orders extending to 2028 and 20–25% revenue growth, neither multiple looks dramatically stretched if you believe the cycle has durability. The risk is the other side of the lock-in: what happens to pricing and volumes when the current multi-year agreements expire, and whether SSD technology eventually displaces high-capacity HDDs at the density levels AI requires.

LITE is a sharper question. A forward P/E of ~67x against a hardware sector median of ~22x means the market is pricing Lumentum as a high-growth technology platform, not an optical components manufacturer. The company itself has set a target of $2 billion in quarterly revenue with 40% non-GAAP operating margins within 18–24 months — roughly 2.5x the current quarterly run rate. Achieving that requires flawless execution on several simultaneous ramps: EML output, co-packaged optics volume, optical circuit switch deployments, and a new indium phosphide fabrication facility in North Carolina beginning production in 2028.

Resilience Under a Geopolitical Shock

The Iran war provides a live test of how these stocks behave when macro conditions deteriorate sharply. US-Israel strikes on Iran began on February 28th. In the weeks that followed, oil surged, gold sold off, equities weakened, and credit spreads widened. Most of the broad market gave up its 2026 gains entirely.

Storage held.

In the period since the Iran strikes, STX returned +2%, WDC returned +10%. SPY returned -4.5% over the same window. NVDA -1.5%. Gold, often treated as a geopolitical hedge, returned -16%. Oil was the obvious war beneficiary at +44% — but within equities, the storage names held and extended while everything else retreated.

The Coherence Signal on STX remained LONG through the entire war period without interruption. WDC maintained its Coherence Signal positive throughout, cycling in and out of the Qualifier Signal. LITE’s Coherence Signal stayed positive through the full period. None of the three approached a Coherence Signal break.

The reason is structural insulation. The demand driving Seagate and Western Digital is not sensitive to energy prices, consumer confidence, or near-term economic growth. It is sensitive to one variable: whether the hyperscalers continue building AI data centers. Those companies have signed binding multi-year purchase agreements that do not reset because of a conflict in the Persian Gulf. War changes oil supply. It does not change a server procurement schedule that was locked in at the board level two years in advance.

Lumentum has more direct energy exposure through manufacturing and data center operating costs, but the demand signal from hyperscaler optical commitments is similarly insulated from geopolitical noise at this scale.

The Copper Question

On March 17th, Nvidia CEO Jensen Huang confirmed that upcoming Nvidia platforms will keep using copper-based connections alongside optical technologies. LITE sold off in premarket before recovering the same session. The market’s nuanced reaction was correct.

This was not a technology reversal. Nvidia invested $2 billion in Lumentum two weeks prior and signed multi-year purchase commitments. What Huang described is a phased transition: copper at 200G per lane inside the rack works today; co-packaged optics and optical circuit switches are being deployed at higher aggregation layers first, with full CPO adoption in volume not expected until 2027–2028. Lumentum’s own management confirmed at the OFC 2026 conference that the company is currently undershipping demand by 25–30%.

The copper stance is a timing question, not a direction question. The optical transition is happening. The question for the stock at a 67x forward multiple is whether it happens on Lumentum’s 18–24 month schedule or stretches to 30–36 months. That distinction is worth a significant amount of multiple compression or expansion.

What the Signal Can and Cannot Answer

The Coherence Signal is still positive on all three names. Nothing in the price structure has broken. STX is the cleanest — both the long-arc structural signal and the Coherence Signal are positive, Qualifier Signal clear. WDC and LITE carry active Qualifier Signal blocks, but the underlying Coherence Signal has been continuously positive through the full run.

The signal will report when the price structure changes. What it cannot tell you is whether the current price is the right price for the structural story. That requires a view on AI capex durability, HDD technology longevity, optical transition timelines, and execution at three very different companies. None of that is in price structure.

The honest takeaway: Coherence Signal identified a re-rating before it happened. The re-rating has occurred, at extraordinary speed and magnitude. The Coherence Signal continuing to be positive means the price structure has not broken. It does not mean the price is right.

STX and WDC’s forward multiples leave room for the structural story to keep compounding — if the purchase orders through 2028 hold and revenue growth sustains. LITE’s forward multiple of roughly 60x leaves very little room for execution to slip. If the $2B quarterly target takes 30 months instead of 18, or if the optical transition timeline stretches, the multiple compresses materially before the earnings arrive.

The Coherence Signal will report when the price structure changes. The questions above are not signal questions. They are judgment calls about execution, technology adoption timelines, and whether three companies can deliver on the most ambitious financial roadmaps in their histories — simultaneously, in an environment where the broader market is already short.

Thresher Fixed LLC. This is not investment advice.