Curve Steepener. Same Hole. Deeper Water.

Think two to three times before putting on a curve steepener

Curve Steepener. Same Hole. Deeper Water.

This is the third in a series. Links to the previous posts below.

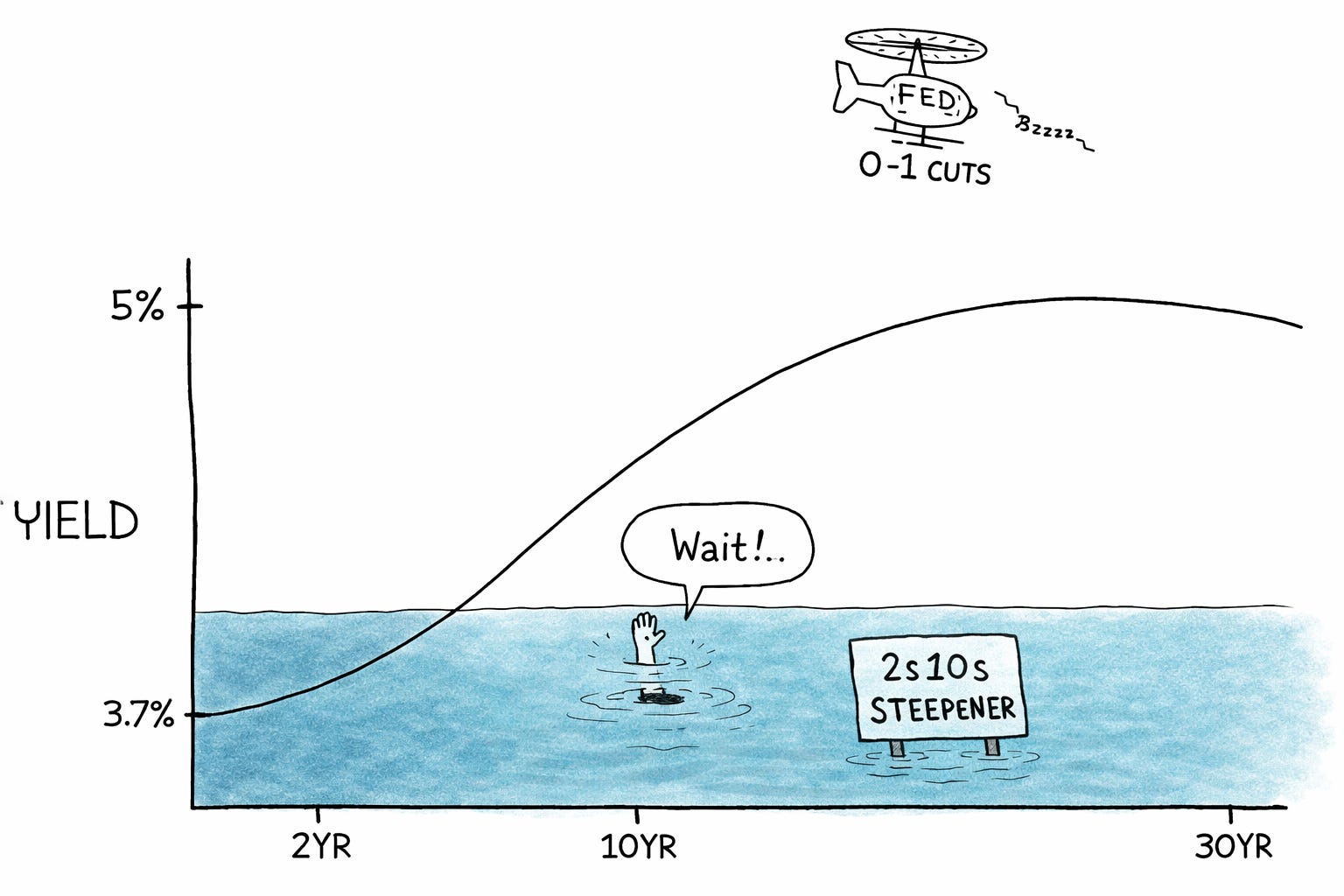

Maybe the third time’s a charm. I’ve written two posts on the curve steepener in the last seven months. Each one carried a warning. The front-end steepener is now actually flat carry but it’s still a bad trade. The curve is flatter than when I last wrote. That’s new. For the first time in this series, the steepener has failed on both dimensions. The carry has been negative every month since the inversion peaked. Now the direction is wrong. The 2s10s curve hit 71bps in January. It’s back to 49bps today. If you put the trade on after reading my December post, you lost carry and gave back spread.

The rolling return on the risk-neutral steepener is negative from every single monthly entry point in my data going back to August 2024. Every one.

The 2026 steepener trade had one real engine: the Fed cutting aggressively enough to drag the front end down while the long end stayed elevated. That thesis is now priced out. Fourteen of nineteen Fed participants see zero or one cut this year. The longer-run rate ticked up to 3.1%. Powell described the rate as “at the high end of neutral.” That is not the setup for a front-end collapse.

What you got instead was a bear flattener. Both ends sold off. The 2-year harder. The curve compressed.

And yet, Morningstar published a piece on March 9th, nine days before the FOMC, calling more steepening “inevitable.” WisdomTree turned the thesis into a product. DoubleLine endorsed it across portfolios. The consensus ran headfirst into the data. The steepener is a story that keeps finding new believers. The carry math doesn’t care.

🔹 If you believe in aggressive cuts, own the 5-year outright.

🔹 If you believe in stagflation, short the long end and own it.

🔹 If you believe in normalization, own risk assets.

All three have outperformed the steepener since August 2024 (by a lot). None of them require you to bleed daily while waiting to be right.

The 2s10s steepener is a great story. It has never been much of a trade. I have now said this three times with real numbers. The numbers keep agreeing with me.

The series so far:

August 2025 — “Beware the Carry Hole”

The original warning. The curve was steepening and the consensus was piling into the 2s10s trade. The math said don’t. To be risk-neutral you need 4x notional in 2s versus 10s, you make 0.4bps for every basis point of steepening, and every day you hold it you bleed carry — the 2-year rolling up toward cash, the 10-year rolling down toward the 2-year. Even in the GFC, with 500bps of cuts and 200bps of steepening, the carry-adjusted return was less than a point. The curve kept steepening after this post. The trade still didn’t work.

December 2025 — “Still a Carry Hole”

Three months later, a progress report. The curve was 7bps steeper since August. The risk-neutral steepener was down 18bps. QQQ was up 10.7%. The alternatives — own the 5-year for cuts, short the long end for stagflation, own risk assets for normalization — all beat the trade that everyone was talking about. The Fed cut 25bps that week. The steepener kept bleeding.

The information contained in this publication is for informational and educational purposes only and should not be construed as investment advice, an offer to sell, or a solicitation to buy any securities, futures, options, or other financial instruments.

The views expressed are the authors’ opinions as of the date of publication and are subject to change without notice. This publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual reader. Readers should consult their own financial, tax, or legal advisors before making any investment decision.

Investing involves risk, including the possible loss of principal.

The authors may hold positions in securities or instruments mentioned and may change such positions without notice. The authors undertake no obligation to update or correct information contained herein.